Investment Idea: Generac is Strategically Shifting Focus to Capitalize on the Data Center Construction Boom, a Pivot that Could Drive 100% Upside Potential within the Next Two Years.

Generac’s Strategy is Pivoting: The company is aggressively shifting its focus from its dominant, but volatile, residential generator market (53.9% of sales) toward the high-growth Commercial & Industrial (C&I) sector. This pivot is driven by the soaring global demand for backup power required by AI infrastructure and new data centers.

Valuation Suggests Upside: The stock currently trades at a premium valuation, indicating the market is pricing in the success of the data center pivot. A normalized valuation model suggests an implied 2028 share price of approximately $371.30, presenting a potential buying opportunity if the company successfully executes its industrial strategy.

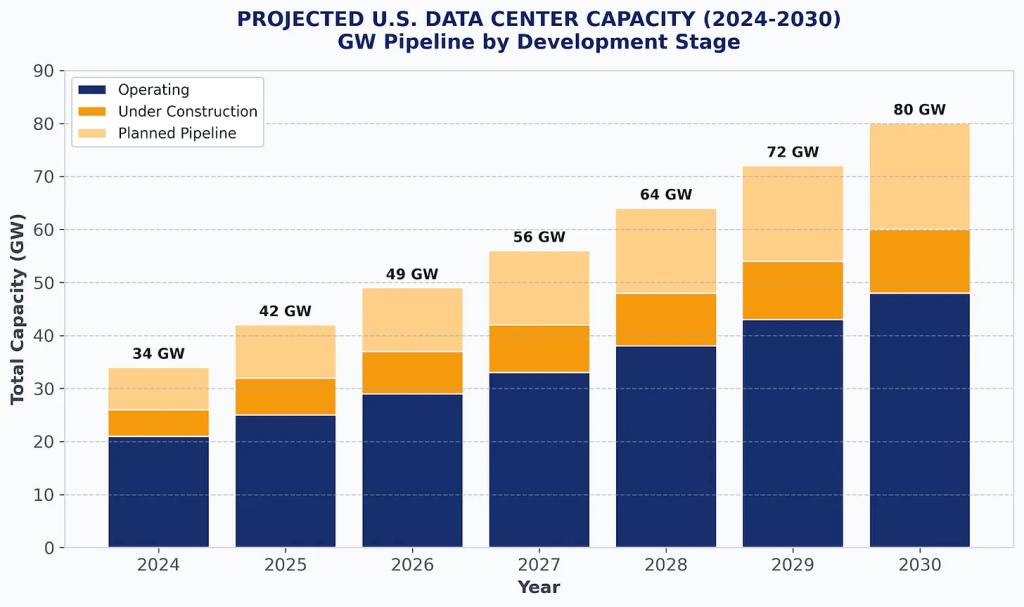

High-Growth Market Opportunity: Generac is positioning itself to capture significant share in the data center backup power market, which is estimated to be worth up to $15 billion annually for diesel generators. The company holds a competitive advantage over rivals like Cummins and Caterpillar due to a significantly shorter generator lead time (30–36 weeks versus 50–70+ weeks) and specialized Modular Power Systems technology.

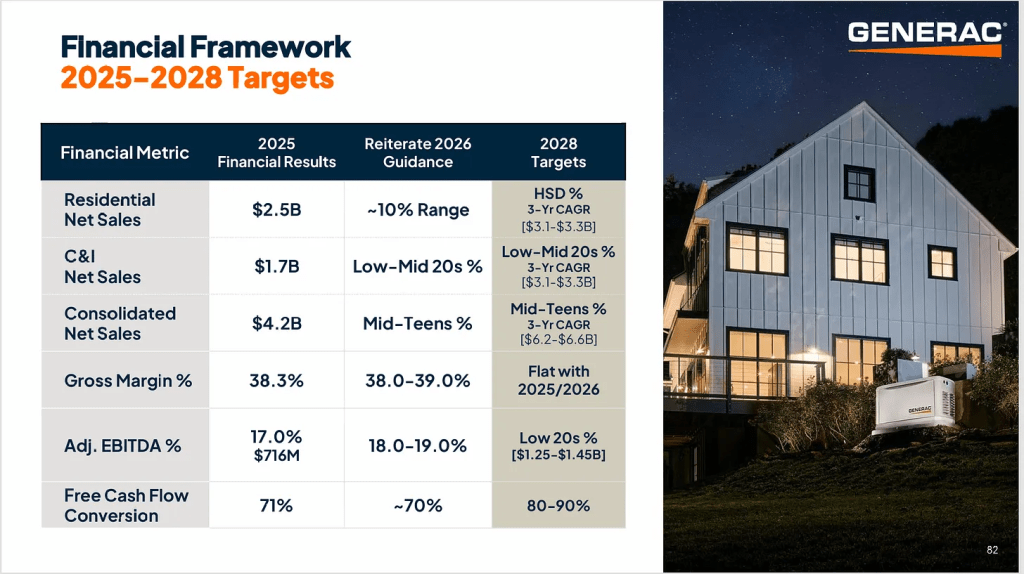

2025 Financial Performance and 2026 Guidance: Total net sales contracted 2.0% in 2025 primarily due to a 7% decline in residential sales, which suffered from a mild power outage environment. For 2026, management forecasts a mid-teens percentage increase in net sales (targeting $4.84 billion), anticipating a 30% expansion in the C&I segment, fuelled by a $400 million data center backlog.

Investment Thesis

Generac’s Strategic Pivot to Data Center Power

Generac Holdings Inc. is strategically pivoting its business model from a reliance on the weather-dependent North American residential generator market, where it holds an estimated 75% market share and currently generates 53.9% of its total sales, toward the high-growth Commercial and Industrial (C&I) sector. This shift is a direct response to the structural volatility in its core residential segment and the soaring global demand for reliable backup power driven by the proliferation of Artificial Intelligence (AI) infrastructure and data centers.

Market Opportunity and Competitive Advantage in C&I

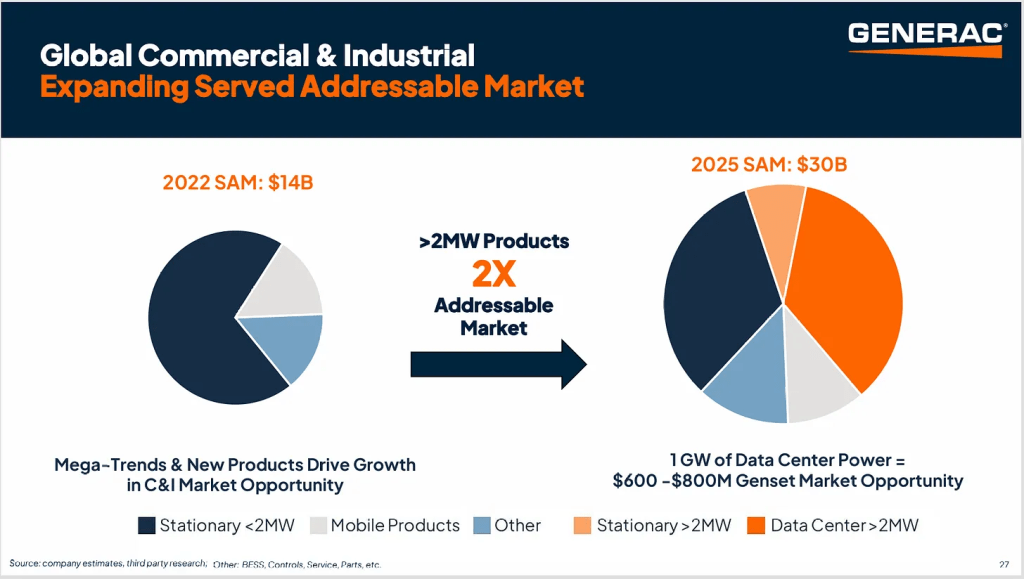

The immense market opportunity in the C&I segment is driven by the mission-critical need for uninterrupted power in data centers, which are required to maintain “Five Nines” (99.999%) uptime for Tier III and Tier IV certifications. Global AI spending, projected to reach over $600 billion in 2026, is spurring an unprecedented build-out of data centers, translating into a massive industrial demand for backup generation. Generac is positioning itself to capture a significant share of this market, which has a potential size of up to $15 billion annually for diesel generators. Its competitive edge over diversified industrial rivals like Cummins and Caterpillar stems from a current lead-time advantage of 30–36 weeks compared to their 50–70+ weeks, as well as proprietary Modular Power Systems (MPS) technology and new high-output diesel platforms (SD1250 and SD1500) optimized for data centers. Management is targeting a 10% to 15% long-term market share in this sector.

Recent Financial Developments and 2026 Guidance

Generac’s financial performance in fiscal year 2025 reflected the challenges of this transition, with total net sales contracting 2.0% to $4.21 billion, primarily due to a 7% decline in the high-margin residential segment caused by a historically mild power outage environment. Conversely, the C&I segment sales increased 4.9% to $1.46 billion, yet this unfavourable sales mix of lower-margin industrial contracts compressed the company’s full-year Gross Margin to 38.30%. For 2026, management forecasts an aggressive re-acceleration, guiding for consolidated net sales to increase at a mid-teens percentage rate, targeting approximately $4.84 billion. This guidance assumes a 30% expansion in C&I sales, fuelled by a $400 million data center backlog, and a 10% recovery in the residential segment. Adjusted EBITDA margin is anticipated to be in the range of 18.00% to 19.00%.

Valuation and Recommendation to Invest

The market is assigning Generac a premium valuation, with a trailing Price-to-Earnings (P/E) ratio of 76.3 and an Enterprise Value to EBITDA (EV/EBITDA) ratio of 25.5, indicating that the equity is being priced on the future success of the data center pivot rather than suppressed 2025 residential earnings. Our analysis has isolated a normalized average EV/EBITDA multiple of 16.8x from the 2022–2025 period to establish a conservative baseline. Applying this multiple to the projected 2028 EBITDA target of $1.35 billion suggests a market capitalization of $21.35 billion and an implied 2028 share price of roughly $371.30. This analysis indicates that the current price level presents a potential buying opportunity, assuming the company successfully converts its commercial and industrial backlog and meets the 2028 EBITDA target.

Brief Description

Generac Holdings Inc., a key player in power generation and energy technology with an $11.79 billion market capitalization, is pivoting its strategy amid soaring demand for AI compute power and data center development. Known primarily as the market leader in North American residential standby generators—a segment where it claims an estimated 75% market share—Generac is significantly ramping up its presence in the industrial generator sector.

The company’s current sales are heavily weighted toward the residential market, which accounts for 53.9% of total sales. Commercial and industrial standby and mobile power equipment contribute 34.7%, with the remainder coming from aftermarket parts and services.

This strategic shift is a direct response to the increasing proliferation of new data centers, which require vast, reliable power generation capabilities to mitigate disruptions. By focusing on the industrial segment, Generac aims to capitalize on the critical need for decentralized power systems essential for maintaining the continuous operation of AI infrastructure.

Industry Positioning

Generac is the market leader in North America for residential standby power systems, a position maintained through sustained historical consolidation in the domestic home standby generator category.

Generac’s core product advantage is the structural integration of traditional mechanical power generation with proprietary, software-enabled energy management technologies. This transition from purely hardware manufacturing to providing comprehensive energy ecosystem solutions is achieved by standardizing Wi-Fi connectivity across the residential line and integrating these systems with the proprietary ecobee smart home platform. Furthermore, the Concerto software platform allows individual residential units to be aggregated into operational Virtual Power Plants (VPPs). This capability transforms the equipment into an active, revenue-generating energy management asset, as end-users can participate in utility grid services and energy arbitrage.

The company’s competitive edge is derived from its robust omnichannel distribution infrastructure, primarily centered on a vast network of independent residential dealers. Competitors, who often have broader and more diversified industrial operations, generally lack the localized density of certified technicians necessary for the complex installation, permitting, and ongoing maintenance of permanent standby power systems.

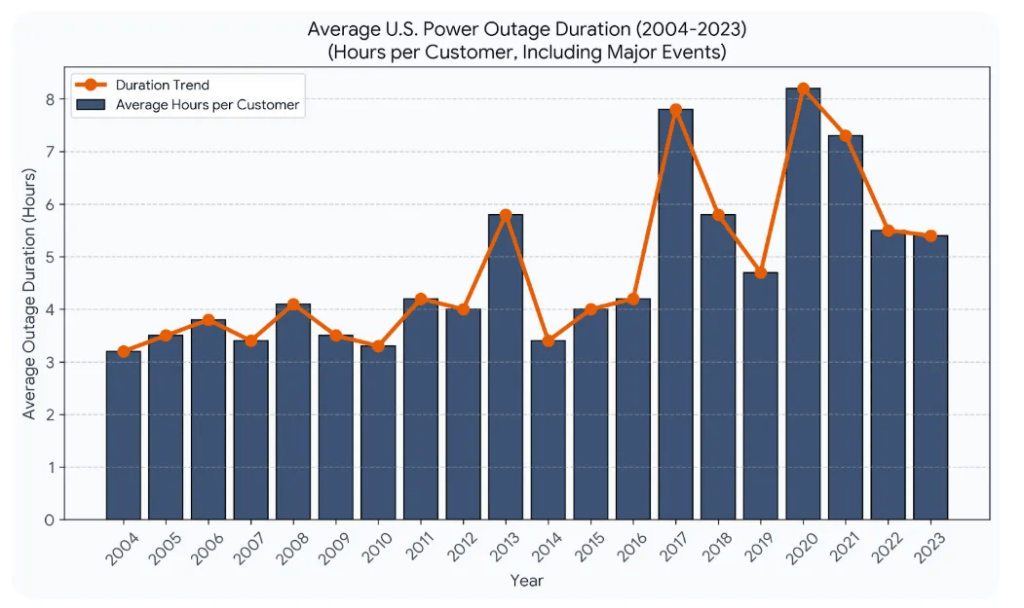

The standby power sector is being structurally driven by two major macroeconomic trends: instability in the residential electrical grid and the build-out of commercial data centers. On the residential side, chronic underinvestment in utility transmission infrastructure combined with an increase in severe climatic events creates a baseline demand for decentralized residential power solutions. Within the commercial and industrial sector, extreme load growth requirements, primarily stemming from the rapid expansion of AI data centers, serve as a significant catalyst for growth.

Sector Analysis

C&I Performance and the AI-Driven Data Center Market Opportunity

Generac finds itself at an inflection point as the industrial manufacturing sector growth relies on AI infrastructure spending. According to the company’s fourth-quarter 2025 earnings report, global Commercial and Industrial (C&I) product sales rose 10% year-over-year to $400 million, while full-year 2025 C&I sales increased 5% to $1.46 billion. Global AI spending, projected to reach $600+ billion in 2026, is spurring an unprecedented build-out of data centers that require massive, uninterrupted power loads. This macro driver directly translates into industrial demand for heavy-duty backup generation. Generac is experiencing an increase in demand for large megawatt generators, which led to the acquisition of additional manufacturing capacity in Wisconsin to double its C&I sales capacity over the next three to five years.

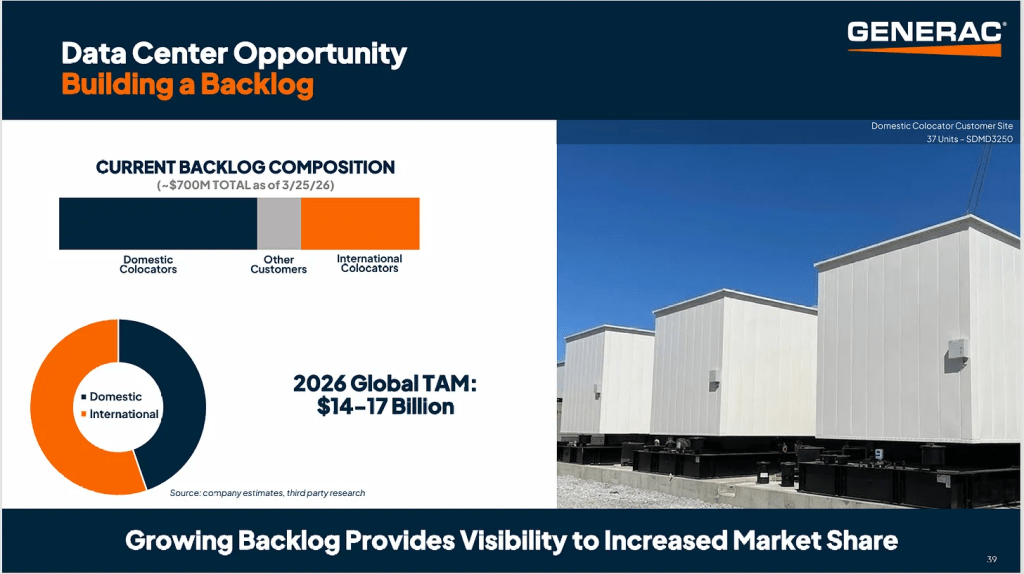

Generac’s strategic pivot toward heavy industrial infrastructure is anchored by a rapidly expanding data center backlog, which reached approximately $700 million as of late March 2026. Management estimates the global total addressable market for these mission-critical power systems will scale between $14 billion and $17 billion in 2026 alone.

The Mission-Critical Imperative for Backup Power

The primary reason data centers require massive industrial generators is to guarantee continuous power supply during grid outages, preventing catastrophic data loss, hardware damage, and severe financial penalties. The industry standard for commercial data centers is to achieve “Five Nines” of reliability, or 99.999% uptime, which translates to allowing no more than approximately five minutes of downtime per year. While Uninterruptible Power Supply (UPS) battery systems are used to bridge the immediate gap when a utility grid fails—providing power for mere minutes—heavy-duty diesel or natural gas generators are required to provide the sustained, long-term electricity needed to run critical IT loads and cooling systems for hours or even days until grid power is restored

Every commercial, hyperscale, and colocation data center globally relies on backup generators. The Uptime Institute, the globally recognized authority on data center performance, mandates the presence of an engine generator for a facility to achieve even its most basic Tier I certification. As facilities scale up to serve major cloud providers and enterprise clients, the requirements become far more stringent. For a data center to achieve a Tier III or Tier IV classification, it must feature redundant generator configurations—such as N+1 or 2N (fully mirrored) setups—meaning these high-end facilities often house dozens of large-scale generators to ensure there is no single point of failure.

The requirement for data centers to house generators stems from a complex intersection of commercial contracts, industry standards, and regional critical infrastructure laws. From a commercial standpoint, operators are legally bound by Service Level Agreements (SLAs) with their clients that enforce strict uptime guarantees, making backup generation a de facto operational requirement. On a regulatory level, jurisdictions are increasingly categorizing data centers as critical infrastructure. In Europe, for example, the EN 50600 standard legally mandates strict emergency power requirements, dictating that critical facilities maintain generator capabilities to run for 24 to 72 hours without grid support.

Residential Sales Contraction and Margin Compression

For the residential product sales the company reported a 23% year-over-year decline in fourth-quarter , falling to $572 million, while full-year 2025 residential sales dropped 7% to $2.27 billion. Management explicitly attributes this contraction to a softer power outage environment compared to the severe weather events of previous years. This contributed to a compression in Generac’s overall gross profit margin, which narrowed to 36.3% in the fourth quarter of 2025 from 40.6% during the same period in the prior year.

Home Energy Management Strategy Expands Addressable Market

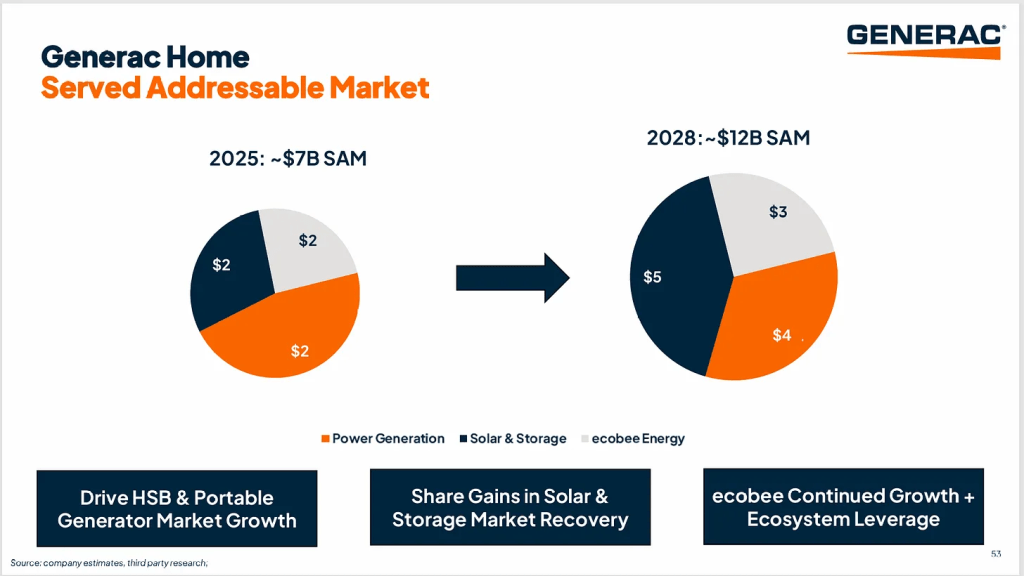

Management projects a substantial expansion of Generac’s consumer-facing market, estimating total growth from approximately $7 billion in 2025 to $12 billion by 2028. This $5 billion projected increase relies heavily on the growth within the “Solar & Storage” segment, which management expects to more than double from $2 billion to $5 billion—becoming the largest single component in 2028. Meanwhile, the legacy “Power Generation” segment, encompassing home standby (HSB) and portable generators, is modelled to grow more modestly from an estimated $3 billion to $4 billion. Additionally, the “ecobee Energy” ecosystem is projected to expand from $2 billion to $3 billion. Ultimately, this quantitative roadmap illustrates Generac’s strategic transition from a traditional hardware manufacturer toward a holistic home energy management and smart ecosystem provider.

Competition

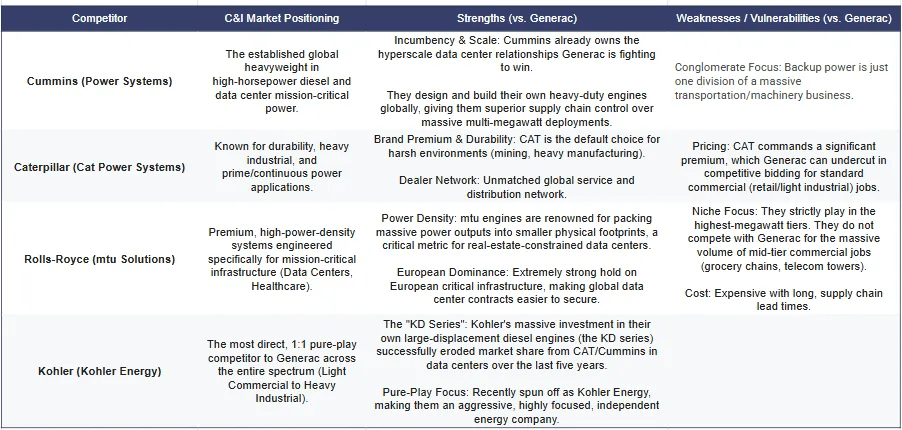

The competition in the power generation and residential standby sector is heavily consolidated among a select group of legacy industrial manufacturers. The top competitors are diversified industrial giants Cummins Inc., Kohler Co., Caterpillar, Rolls-Royce.

Residential Market Share 75%

Generac positions itself as a specialized, pure-play manufacturer of decentralized energy solutions, fundamentally distinguishing its operational model from its diversified primary competitors. This concentrated focus has facilitated the development of a highly specialized, proprietary dealer network that competitors struggle to replicate. This specialized, pure-play operational model directly enables Generac’s outsized domestic market share, as the complex permitting, localized installation, and recurring maintenance requirements of residential standby systems necessitate a dedicated, single-purpose service network rather than generalized industrial distribution channels.

The primary competitive risk in the residential segment involves the “clean energy transition” and the rise of residential solar+storage. Competitors like Sunrun and Sunnova offer alternative resilience solutions that do not require fossil fuels.

Aiming growth in C&I

The selling points of Generac’s industrial portfolio are:

- New products – SD1250 & SD1500, launched in March 2026: These new 46-liter diesel generators are specifically optimized for “mission-critical” environments.

- Modular Power Systems (MPS): Generac’s proprietary MPS technology allows multiple generators to be paralleled without the need for traditional, expensive third-party switchgear. This modularity allows data center operators to scale capacity in “just-in-time” increments, reducing initial capital expenditure compared to monolithic setups.

- Lead Time Advantage: Currently Generac offers open generator set lead times of 30–36 weeks. whereas lead times at the legacy competitors frequently exceed 50-70 weeks for comparable megawatt-class units.

Historically recognized primarily for its dominant market share in the residential standby generator segment, the company is currently executing a strategic pivot to capture market share from legacy industrial incumbents. Generac differentiates its competitive positioning by focusing on modular power systems and newly developed high-output diesel platforms specifically engineered for the thermal and spatial constraints of modern data centers. While the corporation’s absolute market share in the global data center generator sector remains smaller than that of Caterpillar or Cummins, its rate of backlog accumulation indicates rapid market penetration. Generac guided 30% (or around $400m) increase in the C&I segment revenues in 2026 coming from data center products, and is based on the company’s ability to offer competitive lead times and dedicated domestic manufacturing.

Revenue Structure and Drivers

Generac’s revenue composition is shifting structurally, moving away from a primary dependence on weather-influenced residential sales toward long-term industrial infrastructure contracts. The company reports consolidated net sales across three main segments: Residential Products, Commercial and Industrial (C&I) Products, and Other Products and Services. As per the full-year 2025 financial results, the Residential Products segment remains the largest revenue source, while the C&I segment has demonstrated robust, stabilizing growth. The third segment, which includes revenue from aftermarket parts, ecobee smart home subscriptions, and remote monitoring, contributes a supplementary recurring revenue stream.

Historically, the Residential division’s revenue has been driven by severe weather and grid instability, which spur immediate consumer demand for home standby and portable generators. However, this segment is currently weak; residential sales declined by seven percent in 2025 because the third quarter saw the lowest total power outage hours since 2015. Conversely, the C&I segment’s main growth engine is the rapid expansion of global data center infrastructure necessary to support artificial intelligence workloads.

Generac’s consolidated revenue has shown significant volatility over the past three fiscal years. A peak in 2022, driven by post-pandemic grid anxiety, was followed by a sharp deceleration in 2023, where revenue contracted by approximately 11.88 percent to $4.02 billion due to a channel inventory reset. Revenue subsequently accelerated in 2024, growing 6.79 percent to $4.30 billion as field inventories normalized. However, a new period of deceleration occurred in 2025, with total net sales declining two percent to $4.21 billion. Management directly attributes this recent decline to the unusually mild power outage environment, which suppressed residential volume despite the counter-cyclical growth in the C&I business.

The outlook projects an aggressive re-acceleration of revenue growth over the next three years, primarily fuelled by industrial infrastructure deployments. Corporate management has set 2026 guidance, forecasting consolidated net sales to increase at a mid-teens percentage rate, targeting approximately $4.84 billion. This projected growth is fundamentally triggered by the operational ramp-up of the new Beaver Dam, Wisconsin, manufacturing facility, which is expected to scale domestic C&I production capacity beyond $1.00 billion by the fourth quarter of 2026. A secondary, highly probable driver for residential recovery is a return to the historical mean for severe weather events. These dynamics underpin Generac’s projected mid-teens revenue growth for 2026.

Profitability trends and outlook

Generac is currently navigating a transitional profitability environment characterized by significant margin compression in the near term, followed by an anticipated structural recovery driven by industrial volume scaling.

The company reported a contraction in aggregate profitability during the 2025 fiscal year. This development was primarily a function of an unfavourable sales mix, wherein lower-margin commercial and industrial shipments outpaced the historically high-margin residential standby generator sales. Expansion in the forthcoming periods is expected to be structurally driven by operational scale within the commercial and industrial segment.

Generac was forced to record a significant, non-recurring accounting charge of $104.5 million in its fourth-quarter 2025 financial results. This provision was specifically designated to settle a major product liability lawsuit related to its portable generator models. The charge stems from long-running legal and regulatory scrutiny over certain portable generators that featured a defective, unlocked handle design, which led to finger crushing and amputation injuries to consumers. This issue previously resulted in massive product recalls and a $15.8 million fine from the Consumer Product Safety Commission (CPSC) in 2023. The $104.5 million provision represents the corporate financial penalty required to resolve the civil product liability claims.

Balance sheet strength

Generac maintains a structurally sound balance sheet, characterized by ample liquidity and manageable near-term obligations. According to the company’s late 2025 financial data, Generac exited the fiscal year with approximately $340 million in cash and cash equivalents. The company reported total gross debt outstanding of approximately $1.33 billion to $1.50 billion at the close of 2025 and the net debt-to-EBITDA ratio hovers near a manageable 2.1x

Capital Allocation and Cash Flow Analysis

Free Cash Flow Contraction and Working Capital Dynamics

Generac’s FCF profile has experienced significant volatility over the past 24 months, highlighting the capital-intensive nature of navigating shifting end-market demand. According to the company’s 2025 year-end financial disclosures, free cash flow contracted sharply to $268 million, a steep decline from the record $605 million generated in 2024. This compression was primarily driven by a heavier working capital burden—specifically, an accumulation of residential generator inventory caused by a softer-than-anticipated power outage environment in the second half of 2025. Looking ahead to 2026, the underlying FCF dynamic hinges on inventory normalization. Management assumes that as residential stocking levels clear and the C&I backlog is converted into sales, free cash flow generation will stabilize. However, this assumption relies heavily on a return to historical weather patterns and uninterrupted execution in the commercial channel.

Capital Expenditure Accelerates Amid Data Center Pivot

The company is currently undergoing a pronounced capital expenditure cycle, aggressively redirecting investments away from its mature residential base and toward high-growth industrial infrastructure. To capitalize on the artificial intelligence megatrend and a burgeoning $400 million data center backlog, Generac acquired an additional manufacturing facility in Wisconsin in December 2025. Furthermore, the company closed the acquisition of Allmand in January 2026 to bolster its commercial offerings. Driven by these strategic deployments, management expects domestic manufacturing capacity for large megawatt generators to surpass the $1 billion mark by the end of 2026. This indicates a sustained period of elevated capital outlay, meaning investors should not expect CapEx to decrease in the near term; rather, it is being structurally upsized to capture hyperscaler market share.

Dividend History and Forward Distribution Security

Generac currently does not pay a regular cash dividend, management has historically eschewed regular quarterly pay-outs in favour of retaining earnings for organic growth and acquisitions. Based on the current CapEx trajectory and the focus on M&A, the primary assumption within the equity research community is that Generac will maintain a zero-dividend policy through at least 2028, opting instead to return capital to shareholders via equity repurchases.

Aggressive Share Repurchase Strategy and Float Impact

In the absence of a dividend, Generac utilizes open-market share repurchases as its primary mechanism for direct shareholder return. On February 9, 2026, the Board of Directors approved a newly authorized $500 million stock repurchase program, slated to execute over a 24-month period. Given Generac’s current market capitalization—which fluctuated between $12 billion and $13.5 billion in early 2026—and a total outstanding share count of approximately 59.6 million, the new $500 million authorization represents roughly 3.7% to 4.1% of the company’s total outstanding equity and free float.

Outlook and Consensus

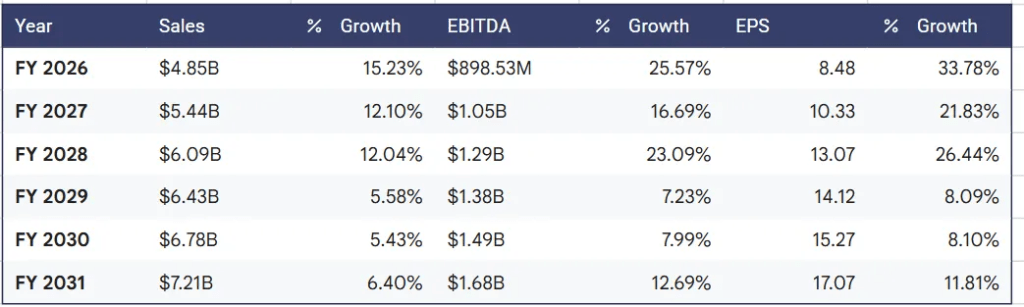

Below are consensus expectations for Sales, EBITDA and EPS as of 25.03.2026

Consensus institutional estimates for Generac Holdings Inc. indicate a projected aggressive growth trajectory for the 2026 fiscal year, heavily reliant on the commercial and industrial data center narrative. Full-year 2026 consensus earnings per share is estimated to be between $8.41 and $8.48, with corresponding revenue estimates positioned between $4.81 billion and $4.85 billion. These institutional figures closely align with the official corporate guidance of approximately $4.84 billion in net sales. For the immediate first quarter of 2026, analysts forecast an earnings per share of $1.29 on revenues of $1.04 billion. The institutional focus has recently shifted: following the release of the fourth-quarter 2025 results in February 2026, multiple brokerage houses raised their price targets despite the corporation missing both top- and bottom-line consensus estimates for the quarter. This indicates a collective institutional pivot toward valuing the enterprise based on its forward-looking data center exposure rather than its trailing residential performance. The current consensus average price target ranges between $222.00 and $245.00.

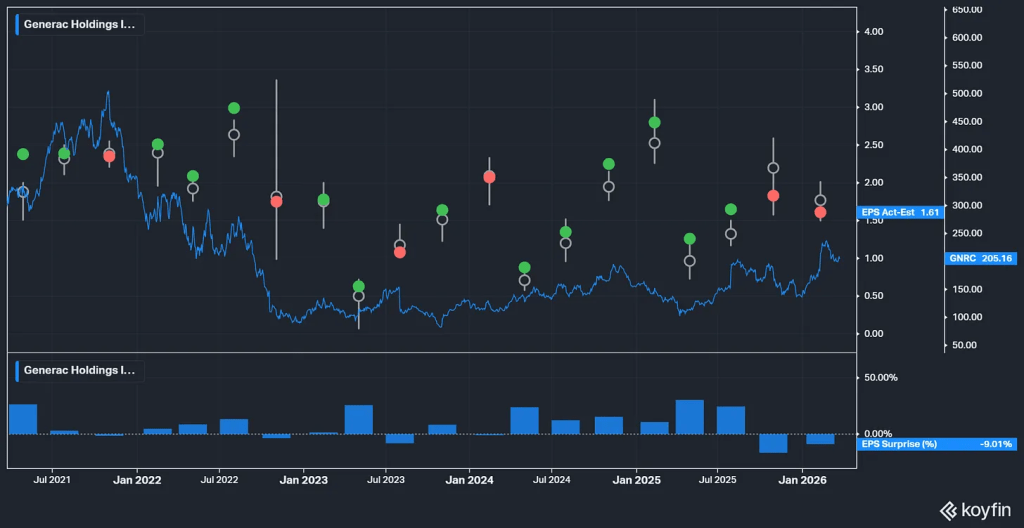

The recent earnings trajectory for Generac has revealed a notable shift from historical institutional outperformance to consecutive misses in the latter half of the 2025 fiscal year. Previously, the company exceeded consensus earnings per share estimates in three of the trailing four quarters. However, financial results for the last two quarters of 2025 indicated sequential underperformance against analyst projections, primarily driven by macroeconomic and environmental factors that negatively affected the core residential segment. This recent pattern of earnings misses suggests a fundamental weakness in institutional forecasting models, which consistently struggle to accurately project quarterly revenue for companies whose sales velocity remains highly dependent on unpredictable, localized severe weather events.

The expansion of C&I segment is expected to improve revenue predictability and dilute the volatility previously associated with the cyclical residential segment.

Guidance Analysis

Generac management forecasts consolidated net sales will increase at a mid-teens percentage rate for the current fiscal year, building on the 2025 baseline. This growth expectation hinges on two key operational assumptions: a projected 30% expansion within the Commercial and Industrial (C&I) segment, largely fuelled by demand from data center infrastructure opportunities, and an assumed 10% recovery in the residential product segment. Furthermore, the company anticipates its adjusted EBITDA margin will fall within the range of 18.00% to 19.00%.

Generac’s History of Guidance Revisions

Generac’s management has a history of mid-year guidance revisions tied to external forces like weather and the economy. In fiscal year 2023, the comoany executed multiple downward revisions, resulting in an 11% annual revenue contraction, primarily due to a severe inventory destocking by its residential dealer network. Conversely, an upward revision was executed in the third quarter of 2024, raising the net sales growth outlook from a 4%-8% range to 5%-9%, a move management attributed purely to unexpected, severe outage activity from Hurricanes Helene and Milton. Most recently, in the third quarter of 2025, the company issued a significant downward revision, lowering the full-year net sales growth expectation from a 2%-5% increase to an approximately flat trajectory due to a historically soft power outage environment.

Valuation

Market Assigns Generac Premium Valuation on Strength of Data Center Pivot

The valuation profile of Generac currently commands a significant growth premium, a direct reflection of strategic expansion into the commercial data center infrastructure segment. Trading at multiples substantially above historical averages as of late March 2026, the enterprise value to sales ratio sits at approximately 3.1, while the enterprise value to EBITDA ratio registers at 25.5. The trailing price-to-earnings ratio is elevated to 76.3. These premium valuation multiples indicate that the market is fully discounting the suppressed earnings from the historically soft 2025 residential outage environment. Instead, it is pricing the equity on the anticipated, execution of the company’s commercial data center backlog.

Normalized Valuation Model Suggests Significant Upside Potential

To establish a conservative valuation baseline, we have isolated the 2022–2025 timeframe, effectively stripping out the extreme residential boom anomaly of 2021. This four-year period, which incorporates both the severe 2022–2023 channel destocking lows and the subsequent commercial data center multiple expansion, yields a normalized average Enterprise Value to EBITDA (EV/EBITDA) multiple of approximately 16.8x.

Applying this conservative, post-pandemic multiple to the projected 2028 EBITDA target of $1.35 billion generates a projected Enterprise Value of $22.68 billion. After deducting the estimated net debt of $1.33 billion, the resulting projected market capitalization of approximately $21.35 billion implies a 2028 share price of roughly $371.30, based on a projected outstanding share count of 57.5 million.

This valuation exercise indicates that even when utilizing a historical multiple that includes the company’s recent operational trough, the math remains skewed toward the upside. Should Generac scale its Commercial & Industrial operations to successfully meet the $1.35 billion EBITDA target by 2028, the current price level presents a buying opportunity.

Risks to Revenue Growth

Generac’s revenue trajectory faces two primary threats: its historical reliance on weather volatility and the operational execution of its commercial pivot. The foremost risk is the company’s dependency on unpredictable severe weather events and associated power outage hours. A notable contraction in residential product sales, which fell 23.00% in the fourth quarter of 2025, was directly attributed to a sustained period of low outage activity compared to prior years. This reliance on weather creates a structural constraint on predictable, linear revenue expansion in the core residential segment. The lack of extreme weather contributed to an overall 2.00% contraction in the company’s total net sales for fiscal year 2025.

A secondary, forward-looking revenue risk is the potential for operational failure in converting the company’s commercial data center backlog—estimated at $400 million—into recognized sales. This execution risk stems from potential challenges such as localized manufacturing capacity constraints or delays in hyperscaler facility construction timelines.

RISKS

Risks to Profitability

Generac’s aggregate corporate profitability faces pressure primarily from a structural shift in its product sales mix and persistent vulnerability to supply chain cost inflation. As the firm scales its Commercial and Industrial (C&I) segment to capture the hyperscale data center market, it is substituting high-margin residential hardware sales for lower-margin, high-volume industrial contracts. This dynamic, compounded by lower manufacturing absorption in the residential segment, directly caused substantial gross margin compression in the preceding fiscal quarter. The gross margin for the fourth quarter of 2025 fell to 36.30%, compared to 40.60% in the fourth quarter of 2024.

Macroeconomic Risks Pose Headwinds to Generac’s Residential Segment

The primary headwind is the restrictive consumer credit environment caused by elevated interest rates, which directly suppresses the total market for residential standby generators by increasing the cost of financing for these large home improvements.

Compounding this risk is the company’s high exposure to geopolitical trade policies and international tariffs. Management cited the impact of higher tariffs as a primary headwind contributing to margin degradation during the third quarter of 2025. Further escalation in global trade restrictions on specialized electronic components or raw materials could force immediate cost inflation across the entire product portfolio, as the domestic supply chain lacks the capacity to replace foreign component volume without significant cost premiums.

What to watch in the next 6-12 month

Generac’s Immediate Outlook Hinges on Data Center Execution and Hurricane Season

Generac faces a critical six-to-twelve-month period defined by two catalysts: the execution of its commercial pivot and the unpredictability of its core residential market.

The primary positive driver is the conversion of its current data center product backlog. Successful deployment of the new SD1250 and SD1500 large-megawatt diesel generators is the key metric for achieving the projected 30% segment growth. Formalizing hyperscaler pilot programs into binding Master Supply Agreements would validate the company’s transition from a weather-dependent hardware manufacturer to a structural infrastructure provider, serving as a significant upward catalyst for the stock.

Conversely, the most significant catalyst for residential segment is the North Atlantic hurricane season, which officially starts in June 2026. Given that Generac’s residential product sales—which totalled $494 million in the first quarter of 2025 alone—remain highly correlated to severe weather events, a structurally calm storm season presents a direct threat to immediate revenue generation.

Selected questions from recent conference calls

Selected questions from 3Q 2025 earning call

- On Data Center Capacity & Backlog: Asked if the capacity expansion and orders are for 2026 or further out, and what the expansion entails.

Answer: Most of the $300 million backlog is for 2026, while hyperscaler conversations are largely focused on 2027 and beyond. To double capacity, Generac is negotiating for new facilities, ordering long-lead testing and material handling equipment, and exploring M&A for additional components.

- On Manufacturing Constraints: Asked about the biggest supply chain or manufacturing challenges in expanding capacity so quickly.

Answer: Production is in Generac’s wheelhouse. Engine supply is not a constraint because their partner (Baudoin) has heavily invested in capacity, and alternator suppliers are known quantities. The main constraints will be physical space and the downstream packaging of enclosures by third parties.

- On Hyperscaler Vendor Lists: Asked about the timeline and process for getting on hyperscaler approved vendor lists (AVL).

Answer: Generac is already a preferred supplier for two global colocators. The hyperscaler AVL process involves intense legal, insurance, and structural vetting. Management described the process as being in the “sixth or seventh inning,” with progress measured in months.

- On Data Center Margins: Asked about pricing and margin profiles for data center generators.

Answer: The average selling price ranges from $1.5 million to $2 million per generator. Margins domestically are similar to the average C&I margins, while international margins are slightly lower. Overall, the incremental impact on EBITDA will be highly positive.

Selected questions from 4Q 2025 earning call

- On Hyperscaler Pilot Progress: Asked for confirmation on the lack of backlog orders and what the pilot phase entails.

Answer: Management confirmed there are no material hyperscaler orders in the $400 million backlog yet. They are in deep negotiations and running pilot programs with two hyperscalers. Assuming successful pilot completions by late Q1/early Q2, they expect to sign master supply agreements for significant volumes in 2027 and 2028.

- On Data Center Competition: Asked if the market opportunity is inviting new competitors.

Answer: The competitive landscape is largely unchanged because high barriers to entry exist around manufacturing large diesel engines. Generac’s engine partner has significant capacity, which provides a competitive advantage.

- On Market TAM and Share: Asked about the data center TAM over the next 3-5 years and realistic market share expectations.

Answer: The data center diesel generator TAM could be as much as $15 billion annually. Generac is targeting a 10% to 15% market share, which aligns with its current North American C&I market share. Capturing just 10% would effectively double their current $1.5 billion C&I business.

- On Penetration Rates: Asked about home standby penetration and multiyear growth expectations.

Answer: The U.S. market is only 6.75% penetrated, and every 1% of penetration represents a $4.5 billion opportunity. Historically, the category has grown at ~15% annually, and management sees a massive runway due to increasing power grid instability.

Selected questions from March 2026 Capital Markets Day

- On Vertical Integration: Asked how far Generac wants to take vertical integration.

Answer: While highly integrated in residential products, Generac will not manufacture large diesel engines for C&I. Instead, they will focus on fabricating structural elements, enclosures, and switchgears (such as through the Enercon acquisition), which alone adds over 100 basis points of margin improvement.

- On Data Center Capacity: Asked if the two potential hyperscaler opportunities are in line with the $1.2 billion capacity or if expansion will be needed.

Answer: Expansion would be necessary. Generac has a $600 million non-binding notice to proceed from one hyperscaler for 2027, and if they win more than one account, they will need to expand beyond their current $1.2 billion capacity.

- On Hyperscaler Requirements and AVL: Asked how confident they are that the product meets hyperscaler demands and how long the Approved Vendor List (AVL) process takes.

Answer: Management is highly confident, as the products have passed reliability and durability testing and outperform competitors due to advanced engine technology. The AVL process was originally expected to take 18-24 months but is being fast-tracked due to the urgent market need for generators.

- On Winning in Commercial Markets: Asked what Generac needs to focus on to win in the commercial business, given their dominance is traditionally in residential.

Answer: Generac focuses on being a purpose-built generator solutions provider rather than a diesel engine manufacturer. They lean on engineering custom solutions for 99.999% uptime and leveraging a robust coast-to-coast service network, successfully replicating their strategy in the telecom sector where they hold roughly 60% share.

- On Gross Margins: Asked why gross margins are modelled as flat from 2018 to today despite the lower-margin C&I segment outpacing residential growth.

Answer: The unfavourable mix (1.5% gross margin impact) is offset by a 2% positive price-cost impact over three years. This positive impact is driven by supply chain resiliency, tariff mitigation, profitability enhancement programs, and vertical integration.

- On the $600M Notice to Proceed: Asked how the $600M notice to proceed factors into the model’s $1 billion data center forecast for 2028.

Answer: It is mostly upside and not fully baked into the model. If Generac completes the AVL process and secures the purchase order, it would provide significant upside in 2026 and 2027.

- On Non-Data Center C&I Growth: Asked about plans for the traditional C&I business if data center strength eventually winds down.

Answer: Generac has separated its sales teams to ensure traditional C&I markets are not neglected. They are already generating backlog for these traditional applications (like cold storage and wastewater treatment) using their newly launched large-megawatt products.