Euqities Suffer Broad Sell-Off, Bond Yields Spike Driven by Surging Crude Prices, and Rising Systemic Credit Stress

United States

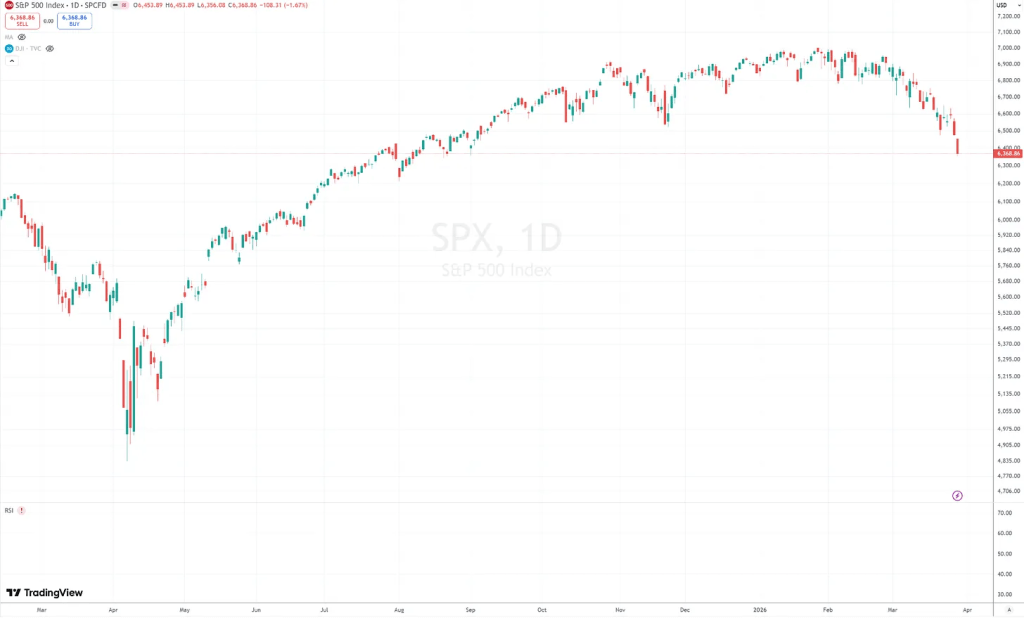

Equities Enter Correction Territory U.S. equities suffered sell-offs over the week, culminating in a fifth consecutive losing week for Wall Street. The S&P 500 declined 1.7% by Friday’s close, marking its most dismal weekly performance since the onset of the current Middle East conflict. Concurrently, the Dow Jones Industrial Average shed 793 points, representing a 1.7% drop that officially pushed the index into correction territory—defined as a 10% decline from its recent peak. This follows the trajectory of the Nasdaq Composite, which fell a further 2.1% to 20,948.36, having already breached the 10% correction threshold earlier in the week.

nergy Markets Surge Amid Geopolitical Strain Commodity markets experienced violent upside volatility as Brent crude eclipsed the $110 per barrel threshold. This represents a premium over the roughly $70 baseline observed prior to the conflict. The market increasingly pricing prolonged disruptions in the Strait of Hormuz.

Treasury Yields Spike on Inflation Fears The fixed-income sector underwent a rapid repricing event, with the yield on the 10-year U.S. Treasury note surging to an intraday high of 4.48% before consolidating at 4.43%. This represents a substantial steepening from the 3.97% yield recorded before the geopolitical escalation. This shift in the bond market underscores a fundamental reassessment of macroeconomic risks and investors are demanding higher premiums based on the assumption that sustained energy inflation will force the Federal Reserve into a more hawkish posture than previously anticipated.

Private Credit Liquidity Constraints Systemic stress is beginning to materialize within the $1.8 trillion private credit market, evidenced by leading alternative asset managers restricting capital outflows. Both Apollo Global Management and Ares Management Corp. formally blocked redemptions. While private credit structures inherently lack the liquidity of public markets, gating these funds explicitly signals that underlying portfolio companies are facing substantial refinancing hurdles and cash flow constraints amid the higher-rate environment.

OpenAI Valuation and Massive Capital Raise Despite the broader market contraction, private venture capital continues to deploy aggressively into foundational artificial intelligence infrastructure. OpenAI is reportedly finalizing documentation to secure an additional $10 billion from tier-one venture investors. This capital injection brings the aggregate funding for its current round to an estimated $120 billion.

Europe

European Markets Navigate Geopolitical Volatility and Resurgent Inflation European equity markets closed a highly volatile week with STOXX 600 a fractional 0.2% contraction as investors grappled with escalating Middle East tensions and a severe crude oil shock that threatens to compress corporate margins. This energy-driven stagflationary risk materialized rapidly in macroeconomic data, notably Spain’s 1% month-over-month CPI surge, prompting fixed-income markets to aggressively reprice the European Central Bank’s monetary trajectory; overnight swaps now indicate a 71% probability of an April rate hike, driving the 10-year German Bund yield to its highest level since 2011.

Germany.

DAX 40 Extends Losing Streak Amid Geopolitical Strain The German equity market faced sustained downward pressure this week, culminating in a 1.41% drop on Friday to push the DAX 40 index down to a close of 22,294. This late-week sell-off cemented a 0.35% weekly decline, extending a severe correction that has erased approximately 11.8% of the index’s value over the trailing four-week period—its most aggressive four-week contraction since early 2022. The primary catalyst remains the escalating Middle East conflict. This external inflationary shock exacerbates Germany’s internal structural challenges, notably sluggish productivity growth, a rapidly aging workforce, and an infrastructure backlog. Rheinmetall AG plummeted 4.34% by Friday’s close, while MTU Aero Engines shed 4.10%. Similarly, technology and infrastructure hardware operators faced severe institutional distribution, with Infineon Technologies and Siemens Energy dropping 3.96% and 3.84%, respectively. The fundamental assumption driving this concentrated sell-off is that surging foundational energy costs and persistent supply chain bottlenecks are rapidly destroying forward operating margins for highly energy-intensive and manufacturing-reliant business models. Chemical giant BASF SE emerged as one of the DAX’s top performers, advancing 2.68% after official corporate data confirmed the successful inauguration of its highly anticipated, fully integrated production site in southern China.

United Kingdom

FTSE 100 Contracts as Energy Shock Exacerbates Domestic Stagflation The United Kingdom’s flagship FTSE 100 index faced correction this week as the escalating Middle East conflict and surging global crude oil prices impaired the domestic macroeconomic outlook. With benchmark Brent crude eclipsing the $110 per barrel threshold, the foundational assumption among investors is that this violent energy shock will aggressively re-accelerate UK consumer inflation, effectively cornering the Bank of England into maintaining a highly restrictive, growth-impairing monetary posture throughout the remainder of 2026. While mega-cap energy producers such as Shell and BP captured concentrated defensive inflows, domestically focused consumer discretionary operators and mid-cap equities within the FTSE 250 suffered acute capital flight due to evaporating demand elasticity. This structural flight to safety reflects a consensus that the British economy remains vulnerable to sustained energy inflation, given its heavy reliance on imported fossil fuels and a fragile consumer base actively absorbing higher foundational living costs.

France

CAC 40 Recoils on Stagflationary Pressures The French equity market sustained elevated institutional distribution this week, with the benchmark CAC 40 index contracting approximately 1.3% to close near 7,950 as escalating geopolitical tensions in the Middle East drove a violent repricing of global risk assets. France’s heavily weighted luxury sector—historically the primary engine for the CAC 40’s outperformance—faced acute capital outflows as macroeconomic anxiety degraded forward consumer sentiment. French spirits conglomerate Pernod Ricard SA captured institutional inflows, advancing approximately 7.0% for the week. This outperformance was catalyzed by official confirmation of preliminary merger discussions with U.S.-based Brown-Forman, the parent company of Jack Daniel’s.

Commodity and FX

Commodity Markets Surge on Geopolitical Strife and Supply Constraints Global commodity markets experienced intense volatility this week, primarily linked to a geopolitical risk premium that drove benchmark Brent crude past the $110 per barrel. This violent energy shock has increased inflation expectations across the macroeconomic landscape, driving up the 10-year U.S. Treasury yield and consequently capping upside momentum for gold, which consolidated near $5,021 per ounce. Front-month COMEX copper futures trading moderately lower to settle near $5.72 per pound with exchange-monitored inventories across the London Metal Exchange (LME), reaching multi-decade highs. U.S. natural gas advanced over 6% to $3.21 per MMBtu partly due to absence of LNG flows through the Strait of Hormuz and partly due to pipeline maintenance bottlenecks. Agricultural complex attracted inflows, driven by disruption of the fertilizer supply chain in the Middle East and increased attractiveness of biofuels in light of surging oil prices.

US Dollar Dominates as Stagflationary Risks Trigger Global FX Repricing The global foreign exchange market experienced a structural flight to safety this week, driving the US Dollar Index (DXY) higher to test the 100.00 psychological threshold. This aggressive dollar accumulation is explicitly anchored by surging crude oil prices and a hawkish repricing of U.S. interest rate expectations; derivatives markets are now factoring in approximately 15 basis points of Federal Reserve tightening for the calendar year, effectively erasing any probability of monetary easing before late 2027. Consequently, risk-sensitive and energy-importing currencies suffered severe depreciations against the greenback. The Indian Rupee plummeted to a fresh record low of 94.82 per dollar, pressured by massive foreign institutional outflows and a widening current account deficit tied to the energy shock, while the Euro sustained accelerated sell-offs as the continental energy crisis exacerbated structural stagflationary fears. The USD/JPY pair aggressively breached the critical 151.00 threshold, driven by the rapid steepening of U.S. Treasury yields. Because Japan operates as a massive net energy importer, the underlying assumption is that sustained crude prices above $110 per barrel will chronically exacerbate the nation’s trade deficit. The British Pound (GBP) retreated sharply against the greenback, sliding toward the 1.2500 support level. The sterling’s structural weakness reflects growing macroeconomic anxiety regarding the UK’s domestic trajectory; as the Middle East energy shock threatens to re-accelerate domestic inflation, markets are pricing in the assumption that the Bank of England will be cornered into maintaining restrictive, growth-impairing monetary policy even as its industrial base contracts.

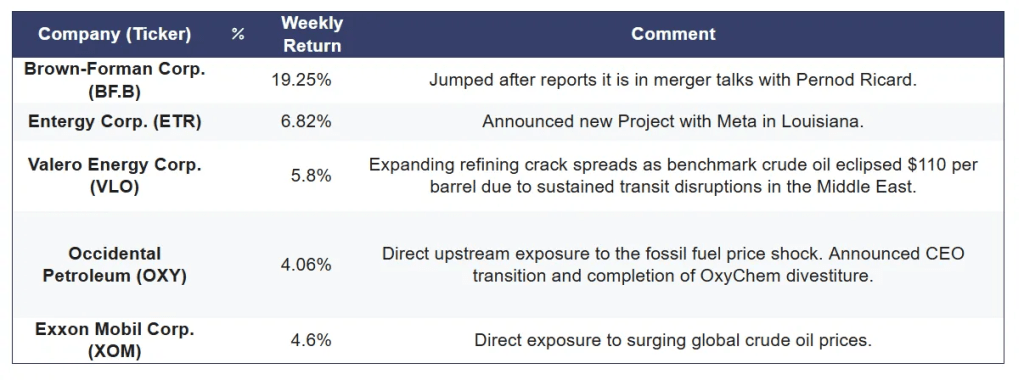

TOP 5 US Outperformers with $10b+ Market cap

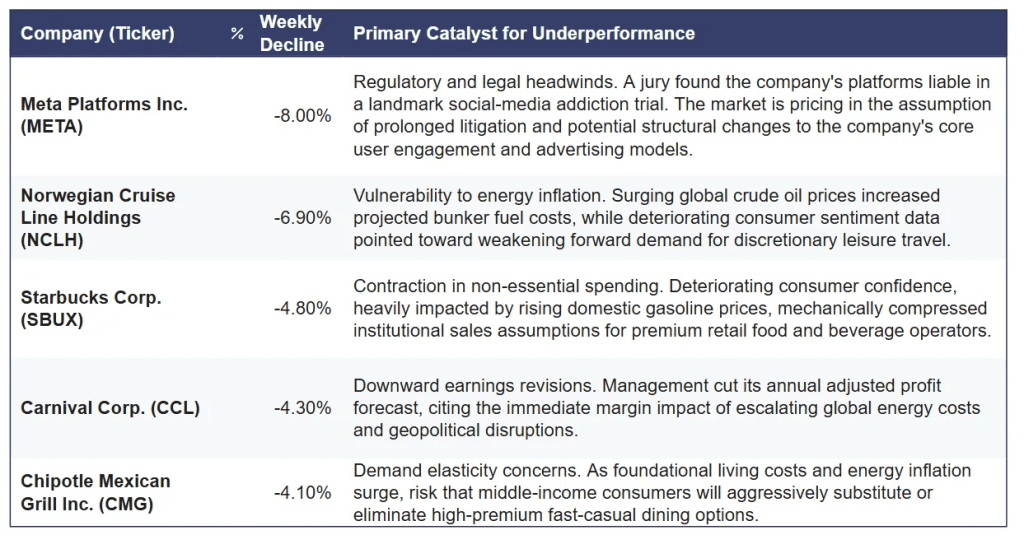

TOP 5 US Underperformers with $10b+ Market cap

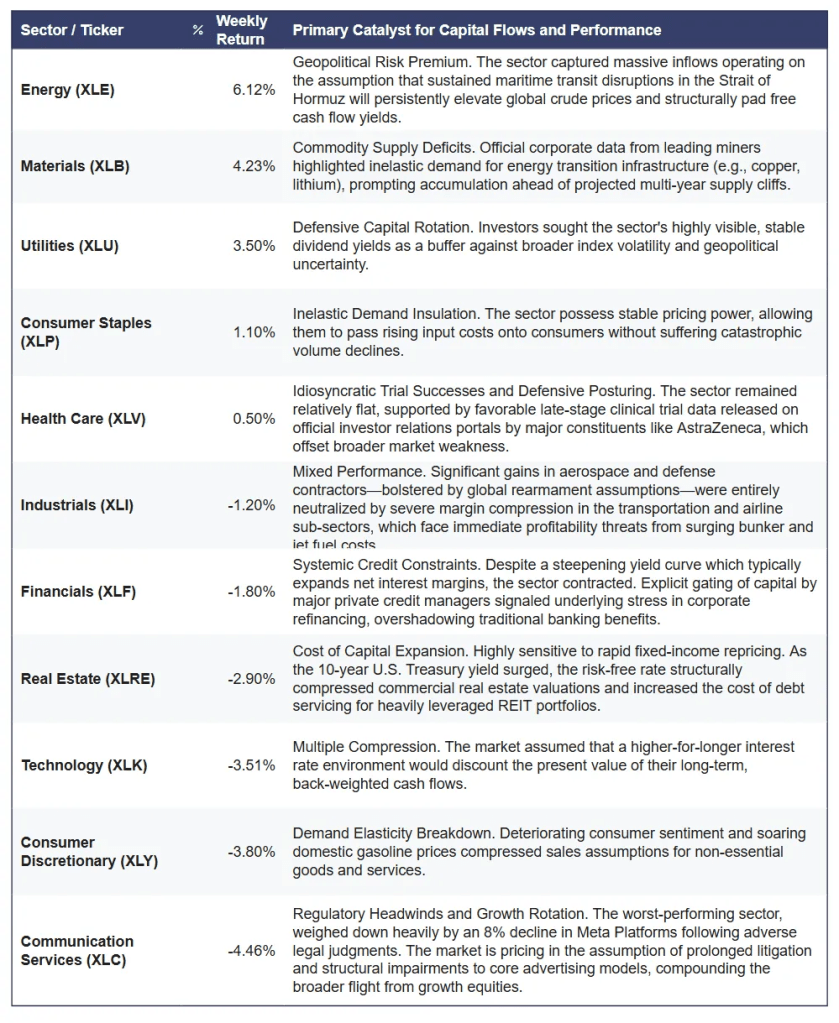

US Sector Performance

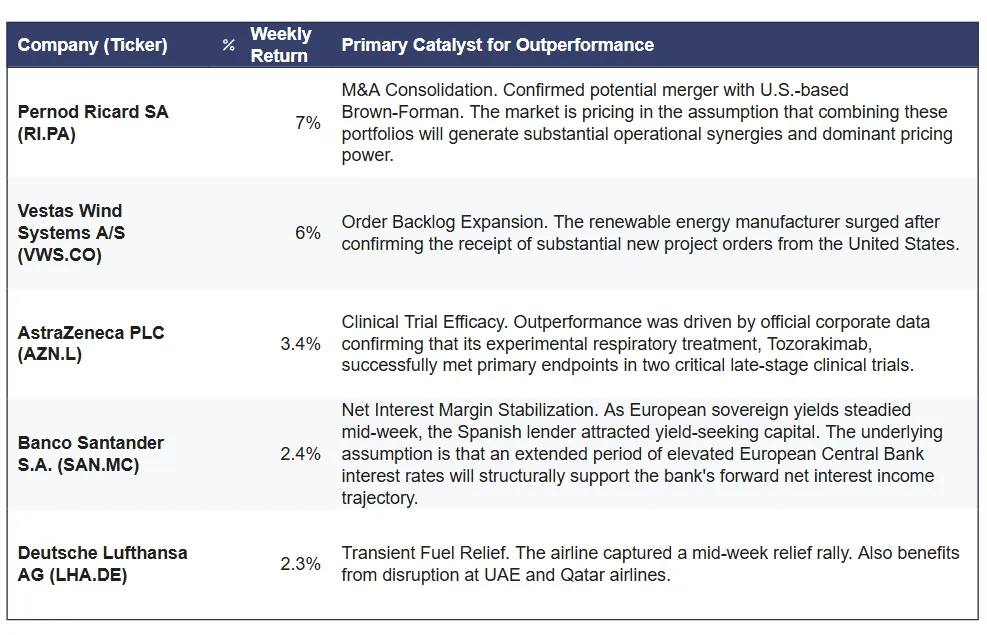

Euro Stoxx 600 Top Outperformers

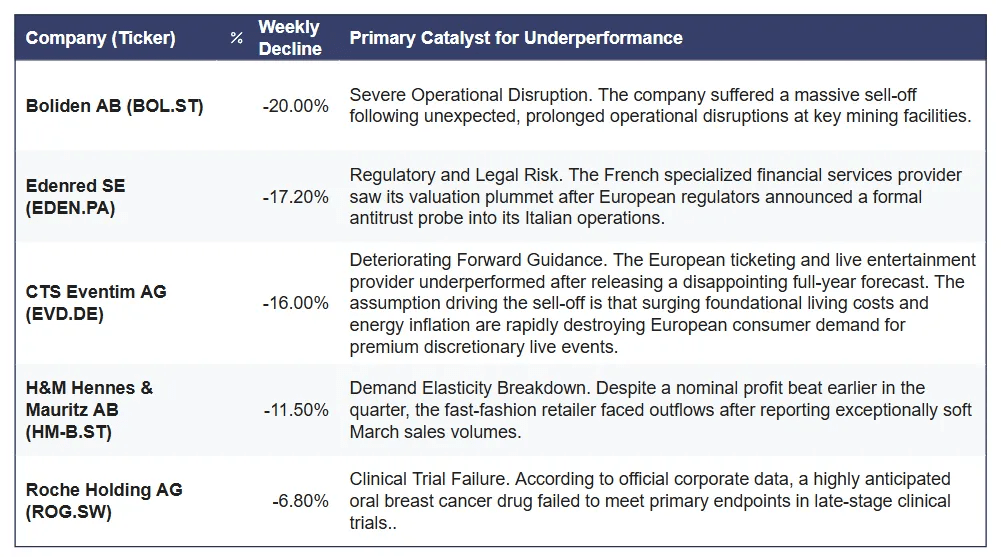

Euro Stoxx 600 Top Underperformers